Events & Promotions

|

|

GMAT Club Daily Prep

Thank you for using the timer - this advanced tool can estimate your performance and suggest more practice questions. We have subscribed you to Daily Prep Questions via email.

Customized

for You

Track

Your Progress

Practice

Pays

Not interested in getting valuable practice questions and articles delivered to your email? No problem, unsubscribe here.

May 01

May 0111:00 AM PDT

-12:00 PM PDT

Free- full-length test + 15 concept videos + 150+ short videos + study plan! Apr 30

Apr 3001:30 AM EDT

-02:30 AM EDT

At one point, she believed GMAT wasn’t for her. After scoring 595, self-doubt crept in and she questioned her potential. But instead of quitting, she made the right strategic changes. The result? A remarkable comeback to 695. Check out how Saakshi did it. May 03

May 0306:30 AM PDT

-08:30 AM PDT

Verbal trouble on GMAT? Fix it NOW! Join Sunita Singhvi for a focused webinar on actionable strategies to boost your Verbal score and take your performance to the next level.

Kudos

Bookmarks

Dropdown 1: 310,000

Dropdown 2: 60%

Be sure to select an answer first to save it in the Error Log before revealing the correct answer (OA)!

Difficulty:

55%

(hard)

55%

(hard)

Question Stats:

67% (02:01) correct 33%

(02:06)

wrong

based on 525

sessions

33%

(02:06)

wrong

based on 525

sessions

History

Date

Time

Result

Not Attempted Yet

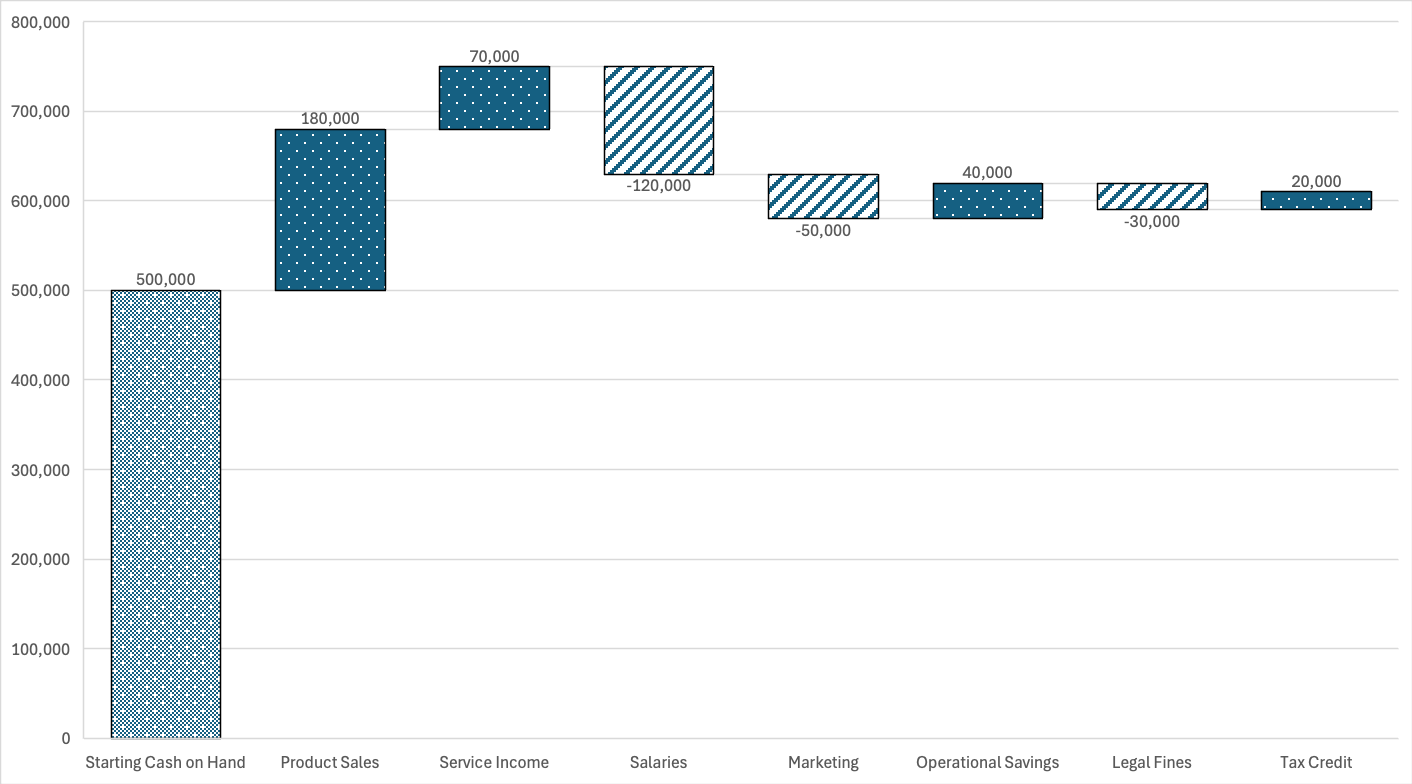

The waterfall chart below illustrates the impact of various business activities on a company’s cash position over the course of a fiscal year. The company begins the year with €500,000 in cash. The chart displays a series of cumulative changes, both positive and negative, arising from seven business activities, ultimately leading to the year-end cash balance.

Positive values (e.g., Product Sales) indicate cash inflows, while negative values (e.g., Salaries) represent cash outflows.

Based on the information in the chart, the total contribution (in euros) from all cash inflow activities to the year-end cash balance is € , and the percentage of total cash outflows attributable to Salaries is closest to .

GMAT-Club-Forum-w599nx6a.png [ 33.57 KiB | Viewed 2471 times ]

GMAT-Club-Forum-jqh0yz7f.png [ 51.71 KiB | Viewed 2192 times ]

GMAT-Club-Forum-k410kkhc.png [ 55.85 KiB | Viewed 2050 times ]

Positive values (e.g., Product Sales) indicate cash inflows, while negative values (e.g., Salaries) represent cash outflows.

Based on the information in the chart, the total contribution (in euros) from all cash inflow activities to the year-end cash balance is € , and the percentage of total cash outflows attributable to Salaries is closest to .

Attachment:

GMAT-Club-Forum-w599nx6a.png [ 33.57 KiB | Viewed 2471 times ]

Attachment:

GMAT-Club-Forum-jqh0yz7f.png [ 51.71 KiB | Viewed 2192 times ]

Attachment:

GMAT-Club-Forum-k410kkhc.png [ 55.85 KiB | Viewed 2050 times ]

ShowHide Answer

Official Answer

Dropdown 1: 310,000

Dropdown 2: 60%

PietroCavallo

Joined: 04 Jun 2024

Last visit: 28 Apr 2026

Posts: 9

Given Kudos: 30

Location: Italy

Schools: CBS '26 (A) Stern '26 (M$$$$) HBS '26 (D)

GMAT Focus 1: 725 Q84 V86 DI88

GPA: 3.65

Kudos

Bookmarks

catinabox

Question, if we talk about 'net contribution' I'm inclined to think that it's only the portion exceeding expenses (e.g., 110). Why it's not simply written 'what is the contribution'? Is this ambiguity also expected on the exam?

Thanks

Question, if we talk about 'net contribution' I'm inclined to think that it's only the portion exceeding expenses (e.g., 110). Why it's not simply written 'what is the contribution'? Is this ambiguity also expected on the exam?

Thanks

Kudos

Bookmarks

I have made some edits to the overall question including the graph.

PietroCavallo