Events & Promotions

|

|

GMAT Club Daily Prep

Thank you for using the timer - this advanced tool can estimate your performance and suggest more practice questions. We have subscribed you to Daily Prep Questions via email.

Customized

for You

Track

Your Progress

Practice

Pays

Not interested in getting valuable practice questions and articles delivered to your email? No problem, unsubscribe here.

Jun 10

Jun 1006:00 AM PDT

-06:15 PM PDT

Register for the GMAT Club Virtual MBA Spotlight Fair – the world’s premier event for serious MBA candidates. This is your chance to hear directly from Admissions Directors at nearly every Top 30 MBA program..

bschooladmit20

Kudos

Bookmarks

| FROM Bschooladmit20 - Current Student: The Next Frontier in Digital Entertainment: Conquering India |

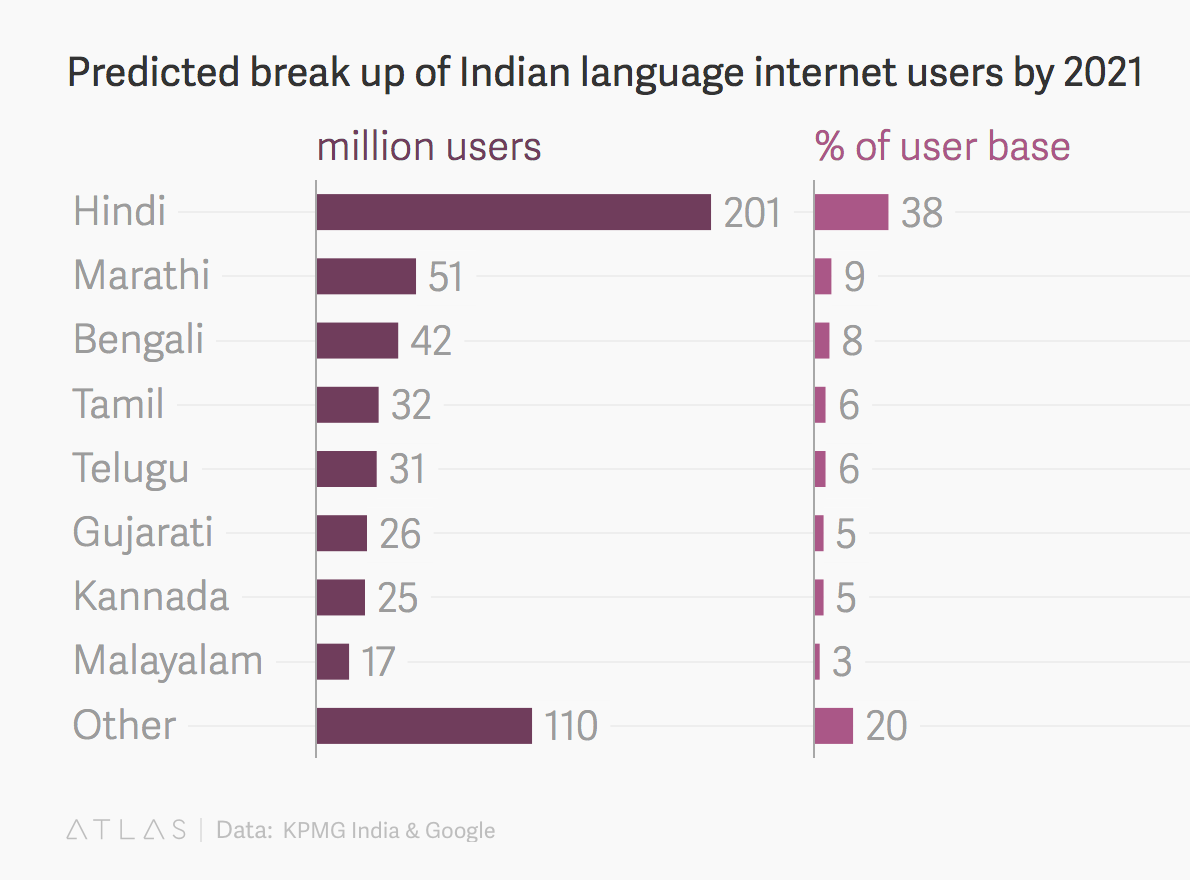

The scale and depth of opportunities presented by the quickly evolving digital entertainment industry in India is astounding. India is an ideal market for new digital entrants. With a population of 1.3 billion and purchasing power of $9.7 trillion, it is unsurprising that both domestic and foreign players are actively working to enter this market. Media giants such as Netflix, Amazon, and Hotstar are investing significant resources to develop strategies for capturing the Indian market. However, none of the current players have managed to gain a significant foothold as yet.We’ve spoken to a range of startups and media giants in the country over the past ten weeks + conducted surveys + in-depth secondary research, in order to better understand the content war brewing in the country. This is what we found: The Market Opportunity Traditional market factors make digital in India an attractive opportunity. To begin with, the country’s media and entertainment industry continues to grow and is expected to reach $34.8 billion by 2021. Internet adoption Contributing to the growing opportunity for digital players is India’s rising internet adoption. In recent years, internet use has grown to an estimated 38%. While this percentage seems low compared to countries like the United States, which boast a 76% penetration rate, when accounting for India’s large population, this still represents nearly 500 million consumers. Additionally, converting the remaining 62% is a large opportunity and makes the market very attractive. Fortunately, digital hopefuls do not have to wait long to receive the benefits of this growth, as penetration is expected to reach the 60% mark by 2020 assuming current trends persist. While there is a large population living with low disposable income, the country’s striking income inequality creates large — in total numbers — middle and upper classes. These classes have been the largest drivers of internet adoption in the country to date. While controversial, this fragmented internet adoption creates opportunities for digital players who now understand that part of their strategy to win this key market is developing solutions accessible to India’s poorer and rural populations. Mobile phone adoption Moreover, increased use of smartphones and cellular data creates new access points for the internet, especially for poor and rural citizens for whom internet adoption is low. The entry of mobile network Reliance Jio by giant Reliance Industries jumpstarted growth in India’s internet use. Since launching in September 2016, the company has “acquired over 100 million users — many connecting to the mobile internet for the first time in their lives.” The introduction of Jio has increased not only the total number of users now accessing online content on their mobile devices, but also the amount of consumption happening on those devices, as the data pricing is now a much lower barrier for price-sensitive consumers. The Evolving Digital Viewer India’s first digital consumers were male millennials who lived in urban areas. However, as internet and mobile penetration increase in the country, the profile of the average digital viewer is shifting dramatically. Between 2016 and 2017, the largest growths in digital usage occurred among three segments: women, older millennials, and rural populations.Women Women, particularly those in smaller cities, are gaining online access at a fast rate. According to Hotstar’s The India Watch Report 2018, women in cities with populations between 1L and 10L increased online usage growth by a magnitude of three between 2016 and 2017 compared to two times growth for women in metro areas and cities with at least one million inhabitants. This trend is attributed to the increased availability of affordable smartphone options, which allows both women and those in rural areas to access online content on their mobile devices for the first time. This increase in women internet users is also important because women wield a great deal of purchasing power, controlling 44% of household spending. Millennials India’s millennial population features strong purchasing power, increased internet access, and sheer volume at over 400 million people. The Indian population is relatively young when compared to other major markets such as China and United States. In fact, according to Morgan Stanley, India is on-pace to be the youngest country in the world by 2020. In addition, they are more educated and globally connected than previous generations, expecting content and information to come to them rather than needing to actively seek it out as older generations did via print and television channels. With these factors at play, it is unsurprising that millennials, and to a lesser extent Generation Zers, are a driving force in India’s increased digital consumption. With mobile and digital adoption (generally) inversely correlated with age, it is therefore unsurprising that consumer brands are targeting India’s millenial and Gen Z populations as key demographics to capture. Rural India While people in major metro areas saw a 3.5 times increase in consumption, it was in smaller cities where the jump was most pronounced — a whopping 4.3 times the rate of 2016. Debunking popular thought that metropolitan areas are so-called “cities that never sleep” and therefore have higher consumption than smaller areas, our research has proven that overall consumption as well as binge watching are highest in smaller areas, where their populations stay awake much later than those in large urban areas. Changing Consumption Patterns India’s population is increasingly gravitating towards digital media over legacy options in print, TV, and film. According to eMarketer, “digital will take up nearly a third of daily media time in India”. This year, the average adult will spend an estimated 1 hour 18 minutes per day with digital media. Control, convenience and quality The first India Watch Report 2018 has highlighted some interesting shifts in consumer habits. The new generation of consumers prioritizes control and convenience. Online video consumption has grown by 5x in the past year, and web series are gaining traction as viewership numbers for some of these series begin to exceed the most watched online TV shows in India for the first time. Interestingly, the report also notes that over 96% of Hostar’s watchtime came from videos that were over 20 minutes long: which leads us to believe that consumers are willing to invest time in high quality content. In terms of genres, sports and Bollywood films continue to drive the highest engagement, with comedy and drama series coming second. Regional Content A second key shift is the growth of the popularity of regional content. India has over 125 million English speakers: online, English is still India’s dominant language. Elite/affluent viewers (see appendix for a definition of this demographic) primarily consume content in English: this demographic is projected to increase from 8% to 16% by 2025. However, 70% of these users also view content in other languages. Importantly, a recent study by KPMG India Google found that nearly 70% of Indians consider local language digital content more reliable than English content. The regional language OTT market is growing at 60–65% every month, while regional content comprises nearly 45% of India’s overall online video content consumption. Additionally, by 2021, an expected 201 million Hindi users — 38% of the Indian internet user base — will be online, according to the same study.Given the rate at which its demand is growing, regional content is expected to comprise 20–25% of the overall digital consumption in 2018. The shift to creating regional content has just begun, and will be a key driver of growth in of content consumption in Indian markets going forward.Personalised content Another shift in consumption patterns, highlighted through our interviews and consumer survey, was the move from family viewing to individual content consumption. We think this shift is worth noting, as the move from a family-based to private setting creates the opportunity to create more personalized, contemporary content for various demographics. The Current Landscape Domestic Players Like many other countries, India’s digital scene has been targeted by both local and foreign players. Additionally, it includes both legacy players adjusting their business lines to include digital offerings as well as new entrants focusing on digital-first and often digital-only strategies. With over 100 million subscribers, India’s streaming market is estimated at $280 million. As of 2017, the top five over-the-top (OTT) providers were Hotstar, Voot, Amazon Prime Video, SonyLiv, and Netflix. Hotstar (an entertainment platform launched by Star India, one of India’s largest media conglomerates, wholly owned by 21st Century Fox) is far and away the leading provider. Hotstar has 75 million users compared to the next in the list, Voot, which only has 15 million users (though its parent company, Viacom18, claims this figure is closer to 22 million users). As Jonnalagadda notes, “Hotstar, for instance, has the digital rights to HBO shows in the country, and streams Game of Thrones episodes the same day they air in the U.S. That’s obviously a huge pull, as is the fact that Hotstar has exclusive rights to stream cricket and football games in the country.” India is the largest producer of films in the world in terms of quantity: the industry generated $1.9 billion in 2016. Several of the country’s largest studios, such as Dharma Productions and Red Chillies Entertainment, have signed content deals with Amazon and Netflix: as the war for high quality content and recognizable stars heats up in the country. However, these studios are yet to enter the online series content creation market. AltBalaji, a subscription-based video streaming platform launched in 2017, that is a subsidiary of Balaji Telefilms Limited, one of the largest content production houses, and India’s leading television content creator, could be another significant player in the domestic content creation market, given their focus on creating original and tailor-made shows. AltBalaji, a subscription-based video streaming platform, launched in 2017 and is a subsidiary of Balaji Telefilms Limited, one of the largest content production houses in India. AltBalaji, with India’s leading television content creator, could be another significant player in the domestic content creation market, given their focus on creating original and tailor-made shows. The other categories of players worth mentioning in the domestic digital content space are a) startups focused on creating short-form/snackable content and b) online web series targeted towards millennials and mainly distributed through social media such as The Viral Fever, FilterCopy and All India Bakchod. These players typically have been operating for 3–4 years, raised a Series A round, and employ a data-driven approach to content creation. In addition, there is c) user-generated short-form content distributed primarily through Youtube produced in Hindi or other regional languages, and targeted at Tier 2 and Tier 3 city consumers. Both these players are notably different from the legacy production houses for their digital-first and targeted approach to content creation, and culture. International Players The top international (based outside of India) players are Netflix and Amazon. Both players have announced that India is one of their priority markets globally, and are investing millions of dollars into developing original local content. Amazon is producing 20 original series, while Netflix is aiming for 7 this year. Both companies have are also investing aggressively in growing their libraries of licensed Indian content: Amazon has secured the TV rights to Bollywood star Salman Khan’s movies, while Netflix has won global streaming rights for movies produced by Shah Rukh Khan. In 2015, Netflix announced its plan to aggressively pursue its international expansion plans, with India among its targeted markets. Aside from offering more Indian content, its rollout and offering in India is remarkably similar to that of other markets, having roughly the same price of 500 rupees, which is very close to the $7.99 charged in the US and other markets until recently (prices began rolling out to $9.99 starting October 2015). However, it might be the company’s one-size-fits all approach that ultimately leads to its undoing as a viable contender in this increasingly competitive space. Since launching in India, Netflix has not changed its pricing, even as competing offerings entered at lower price points. Additionally, Netflix’s India office is primarily focused on sales & marketing. Their licensing and original content teams sit in Los Angeles: this lack of local engagement could hamper their understanding of India’s complex market. As of this writing, it is industry consensus that Netflix is losing the race in India with only five million monthly users due its high price point and dwindling content library. It will be interesting to see how the company responds to its competitive advantage and market share. Another major factor in Netflix’s decline in India is the entry of Amazon. Amazon is thought to have invested upwards of $2 billion in its India entry since 2016, offering pricing discounts and other incentives to attract users. In addition to being considerably cheaper than Netflix at 999 rupees for an annual subscription (roughly the equivalent of two months with Netflix), Amazon benefits from providing the video service as part of its larger e-commerce bundle. Additionally, this price point is a small fraction of its US equivalent, which would be over to 6400 rupees instead. Amazon has astutely recognized the need to price this market differently from its other locations, slashing its price to compete with lower cost options such as Hotstar and no-cost options such as Voot and pirated content. This strategy has proven successful, with Amazon attracting an impressive 11 monthly subscribers users as of this writing, over double that of Netflix. Overall through, both platforms have low subscriber figures: Amazon had a little more than 600,000 Prime Video users at the end of 2017 while Netflix had 520,000 subscribers. We believe the real threat to Amazon and Netflix in India is Reliance Industries’ Jio. Jio’s parent company has already acquired a 24.9% stake in AltBalaji and a 5% stake in Eros International in 2018, and is currently in conversations with several production houses. The corporate giant is looking to build a foothold in India’s $20bn media & entertainment sector, through original content licensing and regional programming deals, having already reached 130m subscribers through its wireless network. Our Take: Opportunities and Gaps The significant diversity in consumption patterns, based on age, gender, geography and socio-economic status in India also builds the case for the creation of more niche, personalised and highly relatable content.We believe that the ‘one size fits all’ model of Bollywood will not work in the digital entertainment space, as consumers begin to prioritize control and convenience. There is still ample room for new players and approaches, even as the competition for Indian eyeballs heats up. We believe that digital content will need to be increasingly tailored by age, gender and region, as the profile of users coming online changes. We are particularly excited by the opportunity to create more women-focused content that shows women in new roles given their increased (i) numbers online, (ii) literacy rates, (iii) influence in family and society, and (iv) rise of their spending power. We also believe that regional content will overtake English content in the next 2–3 years, as the use of regional language users has grown from 42m to 234m in the past five years, and this growth is projected to continue at 18%, while English language users coming online are projected to grow at 3%, over the next 5 years. On the other hand, we think monetisation of this content will be a challenge amongst this demographic, given the low willingness to pay and low household buying power across rural India. We think there be significant consolidation in the increasingly crowded OTT space, with a handful of players emerging as winners. However, we believe there is space for new content creators, and think building the supply chain/pipeline for talent amongst content producers, will be fundamental.There is an opportunity to move away from the traditional studio model of content production, to streamline a long and expensive process, that has not kept up with consumption patterns, and to support new voices and talent in this quickly changing market. From a storytelling perspective, we are excited by the opportunities for new influencers and the space to tell stories about a rapidly urbanising India: we would bet big on rise of reality TV. We think the demand for more relatable characters will continue to grow. This article was published by Candace Jones (@candacej) & Natasha Malpani, who are both Stanford MBA Class of 2018 students. Over the past ten weeks, they have conducted interviews with several digital platforms in the country, undertaken secondary research and surveyed over 200 consumers of Indian digital content in order to explore the opportunities and challenges presented by this complex market. This project was supervised by Stanford’s ex-Dean. The Next Frontier in Digital Entertainment: Conquering India was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story. |

This Blog post was imported into the forum automatically. We hope you found it helpful. Please use the Kudos button if you did, or please PM/DM me if you found it disruptive and I will take care of it.

-BB

bschooladmit20

Kudos

Bookmarks

| FROM Bschooladmit20 - Current Student: The War for Attention: Conquering India |

|

The scale and depth of opportunities presented by the quickly evolving digital entertainment industry in India is astounding. India is an ideal market for new digital entrants. With a population of 1.3 billion and purchasing power of $9.7 trillion, it is unsurprising that both domestic and foreign players are actively working to enter this market. Media giants such as Netflix, Amazon, and Hotstar are investing significant resources to capture the Indian market. However, none of the current players have managed to gain a significant foothold as yet.We’ve spoken to a range of startups and media giants in the country over the past ten weeks + conducted surveys + in-depth secondary research, in order to better understand the content war brewing in the country. This is what we found: The Market Opportunity Traditional market factors make digital in India an attractive opportunity. To begin with, the country’s media and entertainment industry continues to grow and is expected to reach $34.8 billion by 2021. Internet adoption Contributing to the growing opportunity for digital players is India’s rising internet adoption. In recent years, internet use has grown to an estimated 38%. While this percentage seems low compared to countries like the United States, which boast a 76% penetration rate, when accounting for India’s large population, this still represents nearly 500 million consumers. Additionally, converting the remaining 62% is a large opportunity and makes the market very attractive. Fortunately, digital hopefuls do not have to wait long to receive the benefits of this growth, as penetration is expected to reach the 60% mark by 2020 assuming current trends persist. While there is a large population living with low disposable income, the country’s striking income inequality creates large — in total numbers — middle and upper classes. These classes have been the largest drivers of internet adoption in the country to date. While controversial, this fragmented internet adoption creates opportunities for digital players who now understand that part of their strategy to win this key market is developing solutions accessible to India’s poorer and rural populations. Mobile phone adoption Moreover, increased use of smartphones and cellular data creates new access points for the internet, especially for poor and rural citizens for whom internet adoption is low. The entry of mobile network Reliance Jio by giant Reliance Industries jumpstarted growth in India’s internet use. Since launching in September 2016, the company has “acquired over 100 million users — many connecting to the mobile internet for the first time in their lives.” The introduction of Jio has increased not only the total number of users now accessing online content on their mobile devices, but also the amount of consumption happening on those devices, as the data pricing is now a much lower barrier for price-sensitive consumers. The Evolving Digital Viewer India’s first digital consumers were male millennials who lived in urban areas. However, as internet and mobile penetration increase in the country, the profile of the average digital viewer is shifting dramatically. Between 2016 and 2017, the largest growths in digital usage occurred among three segments: women, older millennials, and rural populations.Women Women, particularly those in smaller cities, are gaining online access at a fast rate. According to Hotstar’s The India Watch Report 2018, women in cities with populations between 1L and 10L increased online usage growth by a magnitude of three between 2016 and 2017 compared to two times growth for women in metro areas and cities with at least one million inhabitants. This trend is attributed to the increased availability of affordable smartphone options, which allows both women and those in rural areas to access online content on their mobile devices for the first time. This increase in women internet users is also important because women wield a great deal of purchasing power, controlling 44% of household spending. Millennials India’s millennial population features strong purchasing power, increased internet access, and sheer volume at over 400 million people. The Indian population is relatively young when compared to other major markets such as China and United States. In fact, according to Morgan Stanley, India is on-pace to be the youngest country in the world by 2020. In addition, they are more educated and globally connected than previous generations, expecting content and information to come to them rather than needing to actively seek it out as older generations did via print and television channels. With these factors at play, it is unsurprising that millennials, and to a lesser extent Generation Zers, are a driving force in India’s increased digital consumption. With mobile and digital adoption (generally) inversely correlated with age, it is therefore unsurprising that consumer brands are targeting India’s millenial and Gen Z populations as key demographics to capture. Rural India While people in major metro areas saw a 3.5 times increase in consumption, it was in smaller cities where the jump was most pronounced — a whopping 4.3 times the rate of 2016. Debunking popular thought that metropolitan areas are so-called “cities that never sleep” and therefore have higher consumption than smaller areas, our research has proven that overall consumption as well as binge watching are highest in smaller areas, where their populations stay awake much later than those in large urban areas. Changing Consumption Patterns India’s population is increasingly gravitating towards digital media over legacy options in print, TV, and film. According to eMarketer, “digital will take up nearly a third of daily media time in India”. This year, the average adult will spend an estimated 1 hour 18 minutes per day with digital media. Control, convenience and quality The first India Watch Report 2018 has highlighted some interesting shifts in consumer habits. The new generation of consumers prioritizes control and convenience. Online video consumption has grown by 5x in the past year, and web series are gaining traction as viewership numbers for some of these series begin to exceed the most watched online TV shows in India for the first time. Interestingly, the report also notes that over 96% of Hostar’s watchtime came from videos that were over 20 minutes long: which leads us to believe that consumers are willing to invest time in high quality content. In terms of genres, sports and Bollywood films continue to drive the highest engagement, with comedy and drama series coming second. Regional Content A second key shift is the growth of the popularity of regional content. India has over 125 million English speakers: online, English is still India’s dominant language. Elite/affluent viewers (see appendix for a definition of this demographic) primarily consume content in English: this demographic is projected to increase from 8% to 16% by 2025. However, 70% of these users also view content in other languages. Importantly, a recent study by KPMG India Google found that nearly 70% of Indians consider local language digital content more reliable than English content. The regional language OTT market is growing at 60–65% every month, while regional content comprises nearly 45% of India’s overall online video content consumption.  Additionally, by 2021, an expected 201 million Hindi users — 38% of the Indian internet user base — will be online, according to the same study.Given the rate at which its demand is growing, regional content is expected to comprise 20–25% of the overall digital consumption in 2018. The shift to creating regional content has just begun, and will be a key driver of growth in of content consumption in Indian markets going forward.Personalised content Another shift in consumption patterns, highlighted through our interviews and consumer survey, was the move from family viewing to individual content consumption. We think this shift is worth noting, as the move from a family-based to private setting creates the opportunity to create more personalized, contemporary content for various demographics. The Current Landscape Domestic Players Like many other countries, India’s digital scene has been targeted by both local and foreign players. Additionally, it includes both legacy players adjusting their business lines to include digital offerings as well as new entrants focusing on digital-first and often digital-only strategies. With over 100 million subscribers, India’s streaming market is estimated at $280 million. As of 2017, the top five over-the-top (OTT) providers were Hotstar, Voot, Amazon Prime Video, SonyLiv, and Netflix. OTT Players Hotstar (an entertainment platform launched by Star India, one of India’s largest media conglomerates, wholly owned by 21st Century Fox) is far and away the leading provider. Hotstar has 75 million users compared to the next in the list, Voot, which only has 15 million users (though its parent company, Viacom18, claims this figure is closer to 22 million users). As Jonnalagadda notes, “Hotstar, for instance, has the digital rights to HBO shows in the country, and streams Game of Thrones episodes the same day they air in the U.S. That’s obviously a huge pull, as is the fact that Hotstar has exclusive rights to stream cricket and football games in the country.” Legacy studios India is the largest producer of films in the world in terms of quantity: the industry generated $1.9 billion in 2016. Several of the country’s largest studios, such as Dharma Productions and Red Chillies Entertainment, have signed content deals with Amazon and Netflix: as the war for high quality content and recognizable stars heats up in the country. However, these studios are yet to enter the online series content creation market. The one standout player in this space is AltBalaji, a subscription-based video streaming platform launched in 2017. The company is a subsidiary of Balaji Telefilms Limited, one of the largest content production houses, and India’s leading television content creator. This platform could be another significant player in the domestic content creation market, given their focus on creating original and tailor-made shows. Media startups The other categories of players worth mentioning in the domestic digital content space are a) startups focused on creating short-form/snackable content and b) online web series targeted towards millennials and mainly distributed through social media such as The Viral Fever, FilterCopy and All India Bakchod. These players typically have been operating for 3–4 years, raised a Series A round, and employ a data-driven approach to content creation. In addition, there is c) user-generated short-form content distributed primarily through Youtube produced in Hindi or other regional languages, and targeted at Tier 2 and Tier 3 city consumers. Both these players are notably different from the legacy production houses for their digital-first and targeted approach to content creation, and culture. International Players The top international (based outside of India) players are Netflix and Amazon. Both players have announced that India is one of their priority markets globally, and are investing millions of dollars into developing original local content. Amazon is producing 20 original series, while Netflix is aiming for 7 this year. Both companies have are also investing aggressively in growing their libraries of licensed Indian content: Amazon has secured the TV rights to Bollywood star Salman Khan’s movies, while Netflix has won global streaming rights for movies produced by Shah Rukh Khan. In 2015, Netflix announced its plan to aggressively pursue its international expansion plans, with India among its targeted markets. Aside from offering more Indian content, its rollout and offering in India is remarkably similar to that of other markets, having roughly the same price of 500 rupees, which is very close to the $7.99 charged in the US and other markets until recently (prices began rolling out to $9.99 starting October 2015). However, it might be the company’s one-size-fits all approach that ultimately leads to its undoing as a viable contender in this increasingly competitive space. Since launching in India, Netflix has not changed its pricing, even as competing offerings entered at lower price points. Additionally, Netflix’s India office is primarily focused on sales & marketing. Their licensing and original content teams sit in Los Angeles: this lack of local engagement could hamper their understanding of India’s complex market. As of this writing, it is industry consensus that Netflix is losing the race in India with only five million monthly users due its high price point and dwindling content library. It will be interesting to see how the company responds to its competitive advantage and market share. Another major factor in Netflix’s decline in India is the entry of Amazon. Amazon is thought to have invested upwards of $2 billion in its India entry since 2016, offering pricing discounts and other incentives to attract users. In addition to being considerably cheaper than Netflix at 999 rupees for an annual subscription (roughly the equivalent of two months with Netflix), Amazon benefits from providing the video service as part of its larger e-commerce bundle. Additionally, this price point is a small fraction of its US equivalent, which would be over to 6400 rupees instead. Amazon has astutely recognized the need to price this market differently from its other locations, slashing its price to compete with lower cost options such as Hotstar and no-cost options such as Voot and pirated content. This strategy has proven successful, with Amazon attracting an impressive 11 monthly subscribers users as of this writing, over double that of Netflix. Overall through, both platforms have low subscriber figures: Amazon had a little more than 600,000 Prime Video users at the end of 2017 while Netflix had 520,000 subscribers. We believe the real threat to Amazon and Netflix in India is Reliance Industries’ Jio. Jio’s parent company has already acquired a 24.9% stake in AltBalaji and a 5% stake in Eros International in 2018, and is currently in conversations with several production houses. The corporate giant is looking to build a foothold in India’s $20bn media & entertainment sector, through original content licensing and regional programming deals, having already reached 130m subscribers through its wireless network. Our Take: Opportunities and Gaps The significant diversity in consumption patterns, based on age, gender, geography and socio-economic status in India also builds the case for the creation of more niche, personalised and highly relatable content.We believe that the ‘one size fits all’ model of Bollywood will not work in the digital entertainment space, as consumers begin to prioritize control and convenience. There is still ample room for new players and approaches, even as the competition for Indian eyeballs heats up. Digital content will need to be increasingly tailored by age, gender and region, as the profile of users coming online changes. We are particularly excited by the opportunity to create more women-focused content that shows women in new roles given their increased (i) numbers online, (ii) literacy rates, (iii) influence in family and society, and (iv) rise of their spending power. We also believe that regional content will overtake English content in the next 2–3 years, as the use of regional language users has grown from 42m to 234m in the past five years, and this growth is projected to continue at 18%, while English language users coming online are projected to grow at 3%, over the next 5 years. On the other hand, we think monetisation of this content will be a challenge amongst this demographic, given the low willingness to pay and low household buying power across rural India. We think there be significant consolidation in the increasingly crowded OTT space, with a handful of players emerging as winners. However, we believe there is space for new content creators, and think building the supply chain/pipeline for talent amongst content producers, will be fundamental.There is an opportunity to move away from the traditional studio model of content production, to streamline a long and expensive process, that has not kept up with consumption patterns, and to support new voices and talent in this quickly changing market. From a storytelling perspective, we are excited by the opportunities for new influencers and the space to tell stories about a rapidly urbanising India: we would bet big on rise of reality TV. We think the demand for more relatable characters will continue to grow. This article was published by Candace Jones (@candacej) & Natasha Malpani, who are both Stanford MBA Class of 2018 students. Over the past ten weeks, they have conducted interviews with several digital platforms in the country, undertaken secondary research and surveyed over 200 consumers of Indian digital content in order to explore the opportunities and challenges presented by this complex market. This project was supervised by Stanford’s ex-Dean. The War for Attention: Conquering India was originally published in Hacker Noon on Medium, where people are continuing the conversation by highlighting and responding to this story. |

This Blog post was imported into the forum automatically. We hope you found it helpful. Please use the Kudos button if you did, or please PM/DM me if you found it disruptive and I will take care of it.

-BB

bschooladmit20

Kudos

Bookmarks

| FROM Bschooladmit20 - Current Student: Bleeding Colour |

You worry about Preserving your sense of self When the women around you Are so defined by their relationships To men You are more than a wife, daughter, mother At first they was asked you when you would marry Now they want to know when you Will give them a child to play with A rented womb Someone once told me They were happy they didn’t Let their daughter work abroad Because it would have been Hard for her to integrate back into society After developing a sense of self She took pride in clipping her wings Before she could learn to fly Another woman told me That she was glad her son Was smart enough to marry a woman Of her choosing That would never challenge him But would take pleasure in Caring for and supporting him She took pride in preserving her sons ego Instead of his mind You worry about bleeding color slowly Always being expected to put Everyone else’s needs before your own Sacrifice is not always the highest value I won’t let you define me. |

This Blog post was imported into the forum automatically. We hope you found it helpful. Please use the Kudos button if you did, or please PM/DM me if you found it disruptive and I will take care of it.

-BB